Full resolution (JPEG) - On this page / på denna sida - Second part - XIV. Credit and Insurance Establishments - 4. Savings Banks. By I. Flodström, Actuary at the Board of Trade

<< prev. page << föreg. sida << >> nästa sida >> next page >>

Below is the raw OCR text

from the above scanned image.

Do you see an error? Proofread the page now!

Här nedan syns maskintolkade texten från faksimilbilden ovan.

Ser du något fel? Korrekturläs sidan nu!

This page has never been proofread. / Denna sida har aldrig korrekturlästs.

1034 XIV. CREDIT AND INSURANCE ESTABLISHMENTS OF SWEDEN.

The savings-banks in Sweden are institutions for public benefit, but of *

private nature, and with an almost unlimited freedom of administration. In this

they differ from those of several other countries, e. g., Great Britain and France,

whose savings-banks must chiefly place their means into the care of the State or

invest them in State bonds; those of Belgium, whose Caisse Générale d’Épargne

et de Retraite is a State institution (which collects savings also through the post

offices, and therefore, in a certain manner, is a P. 0. savings-bank); and those

of the German States, where the administration of the savings-banks is most

frequently an affair devolving upon the community. The first Swedish Savings-Bank

Law, of 1875, ordains that there must be no distribution of dividends in

savings-banks; the law of 1892, now in force, defines a savings-bank as a »financial

institution which, without right for its founders or their assigns to appropriate any

share in the profits which may arise from the business, has for its object to

receive money from the public, to put it out to interest, to increase it still more

by adding the interest to the capital, and to repay the money when notice is

given to that effect», besides which it is ordained that no other financial institution

must carry on its business under the name of savings-bank without special license.

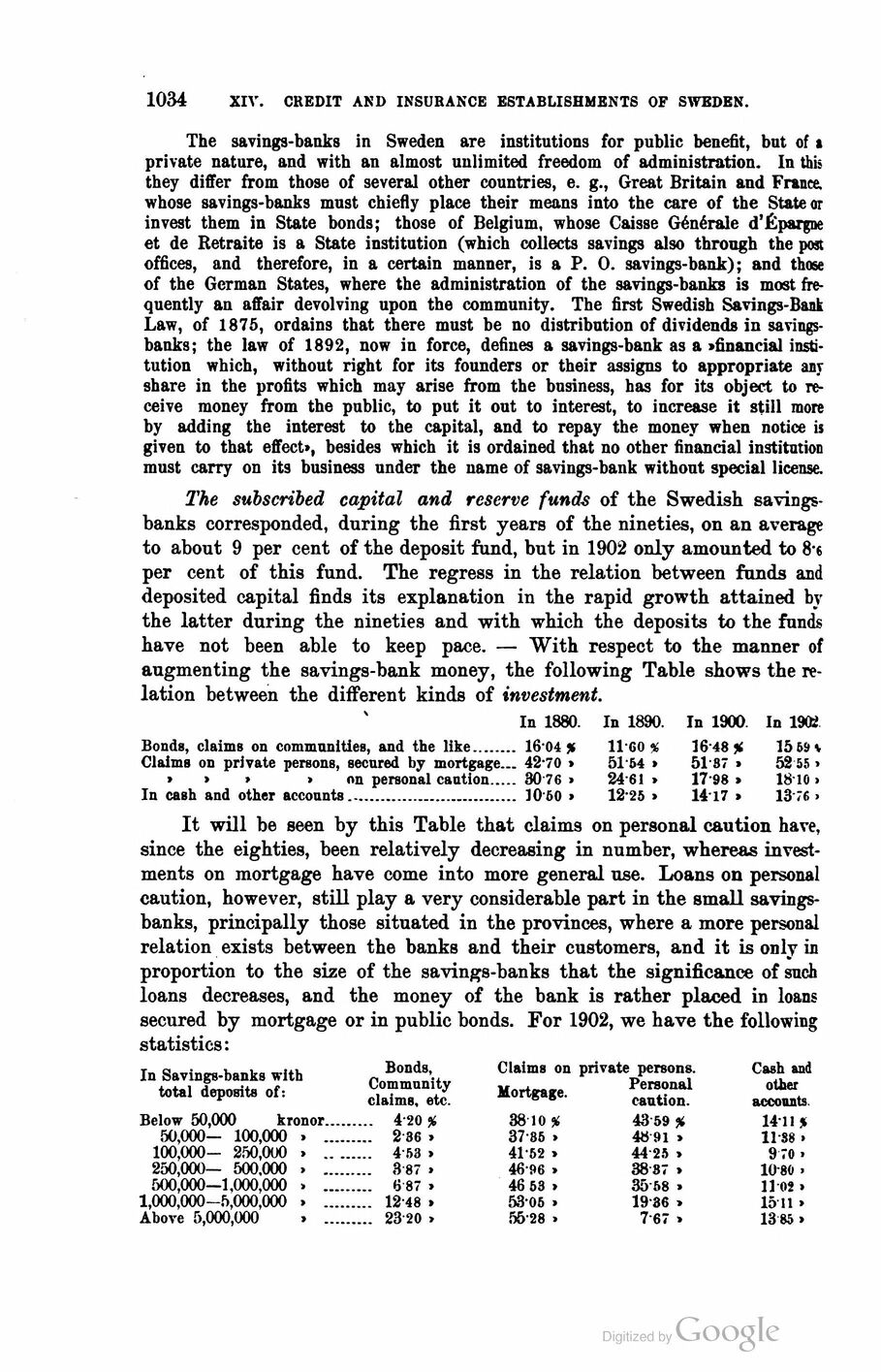

The subscribed capital and reserve funds of the Swedish

savings-banks corresponded, during the first years of the nineties, on an average

to about 9 per cent of the deposit fund, but in 1902 only amounted to 8*6

per cent of this fund. The regress in the relation between funds and

deposited capital finds its explanation in the rapid growth attained by

the latter during the nineties and with which the deposits to the funds

have not been able to keep pace. — "With respect to the manner of

augmenting the savings-bank money, the following Table shows the

relation between the different kinds of investment.

In 1880. In 1890. In 1900. In 1902

Bonds, claims on communities, and the like........ 16-04 % 11-60 % 16 48 % 15 59*

Claims on private persons, secured by mortgage... 42-70 > 51’54 » 5187 » 52 55 >

» > » »on personal caution..... 30 76 » 24 61 » 1798 » 1810 >

In cash and other accounts............................... 10’50 > 12-25 » 1417 » 13’76 >

It will be seen by this Table that claims on personal caution have,

since the eighties, been relatively decreasing in number, whereas

investments on mortgage have come into more general use. Loans on personal

caution, however, still play a very considerable part in the small

savings-banks, principally those situated in the provinces, where a more personal

relation exists between the banks and their customers, and it is only in

proportion to the size of the savings-banks that the significance of such

loans decreases, and the money of the bank is rather placed in loans

secured by mortgage or in public bonds. For 1902, we have the following

statistics:

In Savings-banks with total deposits of: Bonds, Community claims, etc. Claims on private persons. u„ Personal Mortgage. caution. Cash and other accounts.

Below 50,000 kronor 4-20 % 3810 % 43 59 % 1411 %

50,000— 100,000 » 2 36 » 37-85 » 48 91 » 11S8 >

100,000- 250,000 » 4-53 » 41-52 » 44 25 » 9 70 .

250,000- 500.000 » 3 87 » 46-96 » 38 87 » 10-80 .

500,000—1,000,000 » 6 87 » 46 53 > 35 58 » 11 02 »

1,000,000-5,000,000 » 12-48 » 53-05 » 19-36 » 15 11 >

Above 5,000,000 » 23-20 » 55-28 > 7-67 > 13 85 »

<< prev. page << föreg. sida << >> nästa sida >> next page >>

{kind=link}